1. Introduction

Government policies have been instrumental in driving the energy transition in Europe and globally (

Kitzing, Mitchell and Morthorst 2012). Policy instruments like feed-in tariffs and premiums in the past two decades facilitated renewable energy (RE) investments by de-risking their revenues and securing grid connection and electricity offtake (

Couture and Gagnon 2010;

Pahle and Schweizerhof 2016). However, the decline in investment costs (

IRENA 2023) and reduction in cost of capital (

Egli, Steffen and Schmidt 2018) decreased support needs, inducing a scale-back in policy support. Since 2014, under the European Commission’s State Aid Guidelines (

European Commission 2014), European Union (EU) governments have reformed policies to expose RE generators to electricity price risks, encouraging responsiveness to prices and market integration of renewables.

A central element of the new policies is auctioning contracts-for-difference (CfDs), where bidders compete for support contracts primarily based on price criteria (

Fleck and Anatolitis 2023) and in the case of offshore wind for single locations (

Jansen et al. 2022). High competition from leading EU utilities and oil & gas majors and changes to auction designs—such as introducing qualitative selection criteria in Germany and the Netherlands—led to an increasing number of zero bids (

Đukan et al. 2023). When investors bid zero in a CfD auction, they imply they do not need support remuneration and expose their future generation to merchant or electricity price risks.

The auction outcomes depend on CfD designs (

Kitzing et al. 2024). One-sided CfDs allow producers to retain the market upside when electricity prices exceed the auction strike price (

Klobasa et al. 2013). Because investors factor the uncertain market upside into their bids, such CfDs tend to decrease strike prices, often resulting in zero bids (

Đukan and Kitzing 2021;

Đukan et al. 2023), albeit the auction winners gain access to seabed rights. Two-sided CfDs, conversely, remunerate producers when the reference price—typically a time-weighted market electricity price—is below the strike price and claw back any revenues earned when prices rise above this level (see

Annex,

Figure A1). Depending on their design, two-sided CfDs increase revenue stability to varying degrees. For instance, so-called financial and yardstick CfDs (

Newbery 2023;

Schlecht, Maurer and Hirth 2024) also reduce production risks caused by wind intermittency, while standard CfDs with referencing periods remove only price risks (

Kitzing et al. 2024).

Revenue predictability from two-sided CfDs improves financing conditions (

Beiter et al. 2023;

May, Neuhoff and Richstein 2018), particularly in project financing (

Steffen 2018)—one of the primary means for financing Europe’s offshore wind expansion (

Brindley and Fraile 2021). In contrast, zero bids in one-sided CfDs increase merchant risk and worsen financing conditions, raising the project’s capital and electricity generation costs (

Beiter et al. 2023;

Đukan et al. 2023). High merchant risk exposure also deters bidder participation, like the Danish 2024 offshore wind auctions, where the state offered no support remuneration and received no bids (

Wind Europe 2024), underscoring the need for revenue stabilization to support offshore wind build-out.

While many offshore wind markets in Europe—such as the UK, France, and Poland—are already remunerating projects with two-sided CfDs, other major markets like Germany and the Netherlands apply one-sided CfDs (

Jansen et al. 2022). There is, at present, no policy convergence between the leading offshore wind markets in Europe regarding the choice of remuneration scheme, despite the EU Commission’s efforts to make two-sided CfDs mandatory for member states (

European Commission 2023;

Wind Europe 2023). Since the EU plans to increase offshore wind capacity from 27GW in 2021 (

Jansen et al. 2022) to 300GW by 2050 (

European Commission 2020), it is essential to understand the financial benefits and disadvantages of remuneration schemes, one of them being the extent to which they reduce price risks and the effect of this on financing.

Our study contributes to this debate and answers the following research question:

What is the impact of two-sided CfDs on debt sizing for offshore wind farms? Banks adjust their loan exposure in response to anticipated revenue stability (

Bodmer 2014;

Đukan and Kitzing 2023;

Mora et al. 2019;

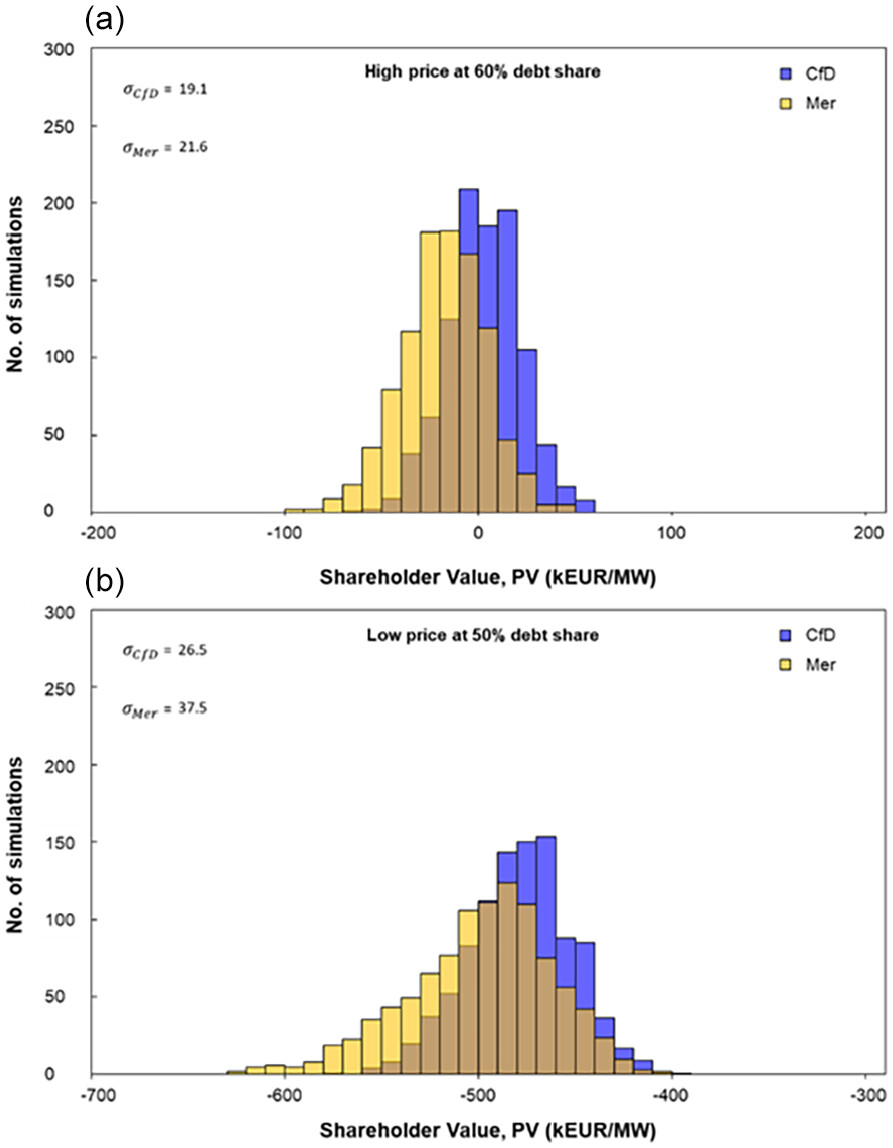

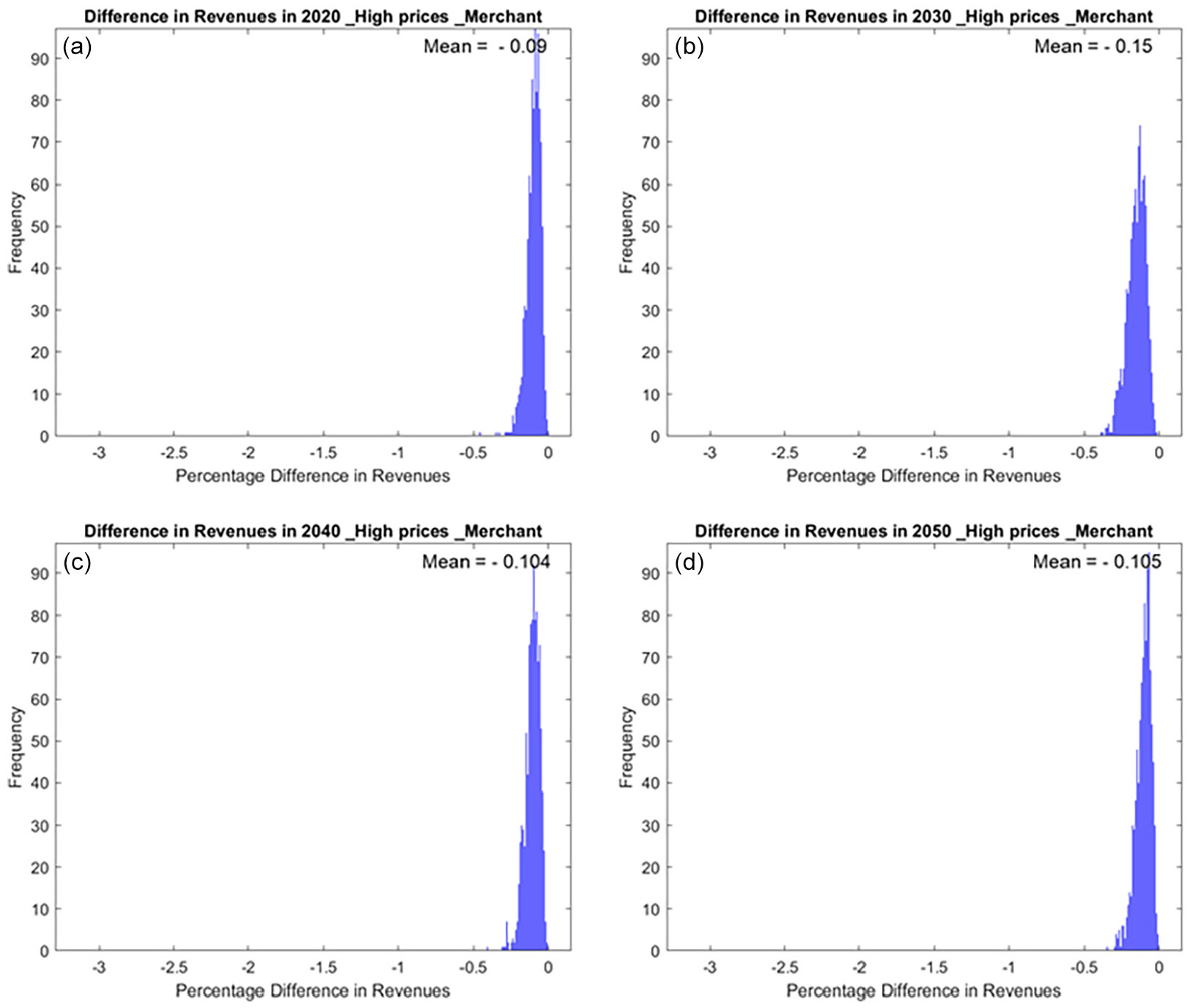

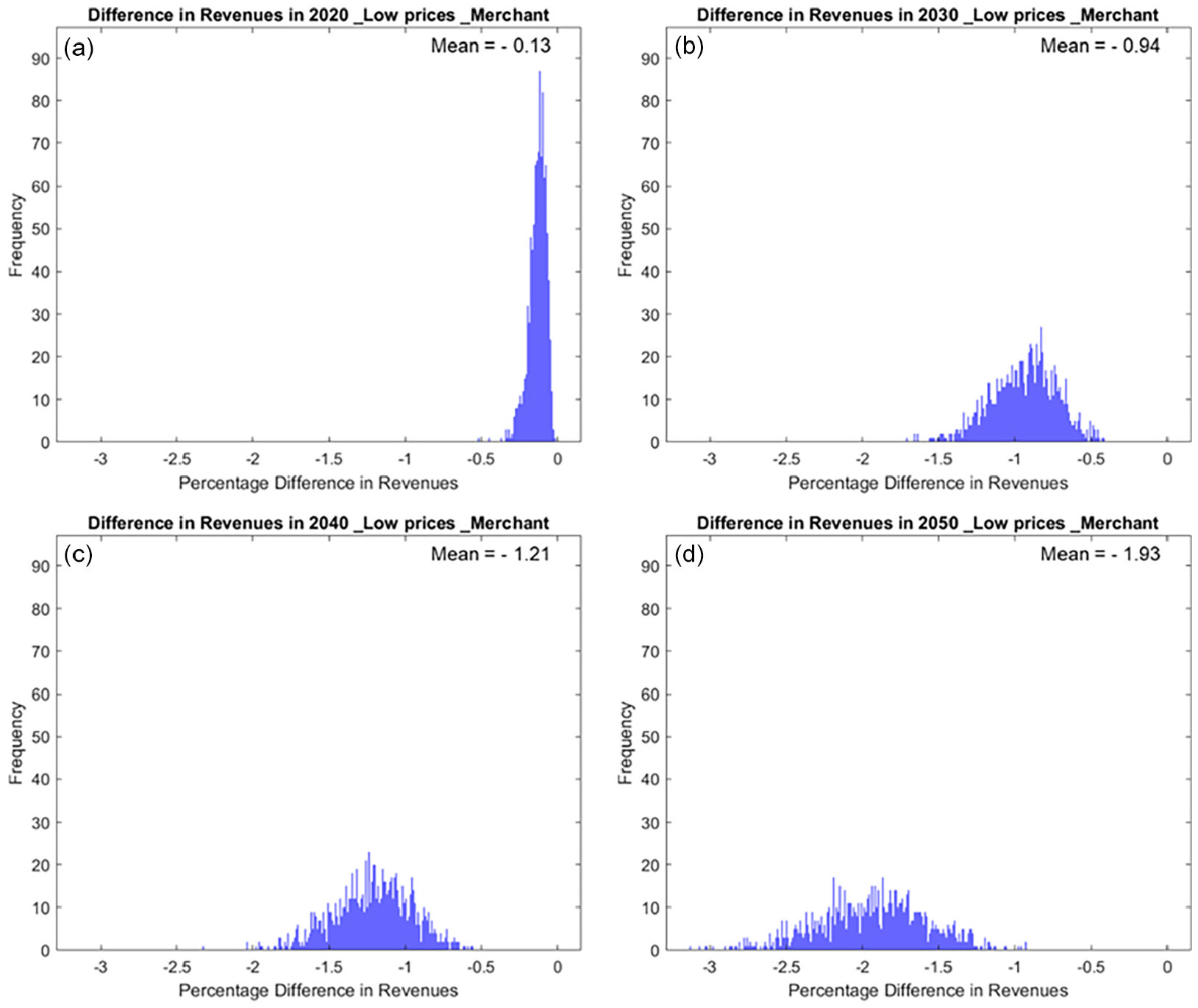

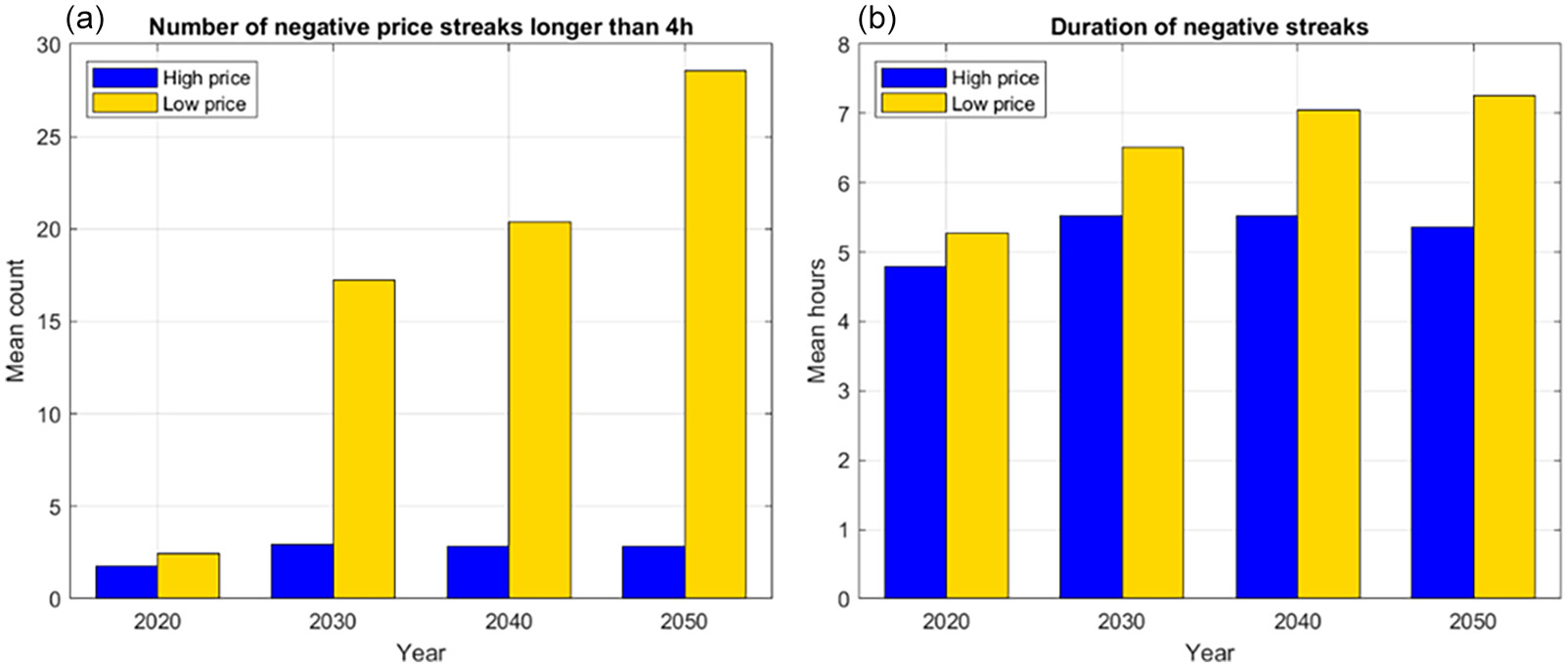

Stetter et al. 2020), making debt size a suitable proxy for price risk and financing conditions in general. To quantify the two-sided CfD impact on debt size, we compare it with selling electricity at wholesale market prices for a hypothetical offshore wind farm in the German North Sea as a case study. Here, we assess a single CfD design with hourly referencing and twenty-year duration, a contract structure frequently implemented in leading EU markets like the UK, and with one of the largest impacts on revenue stability among the considered CfD designs (

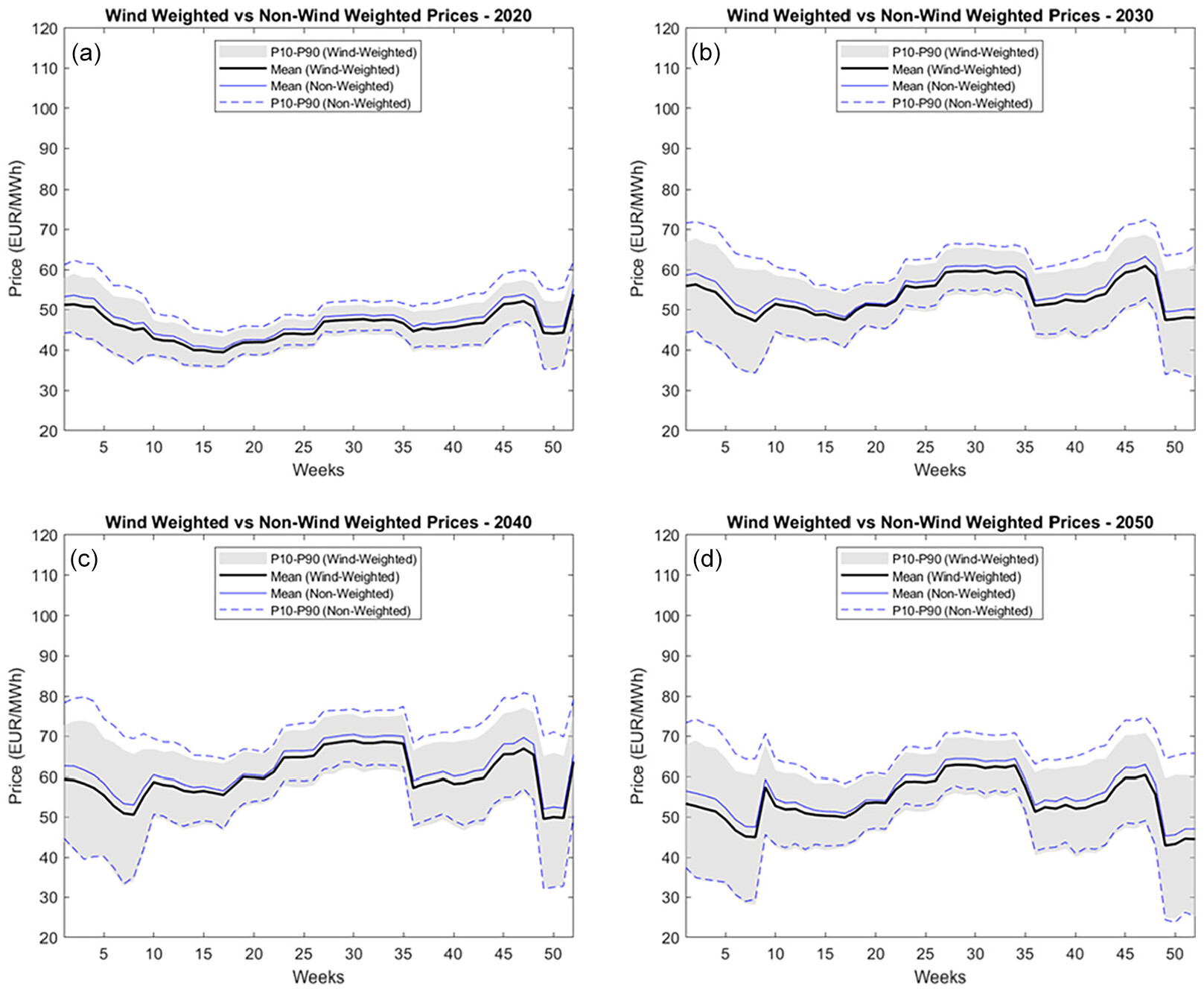

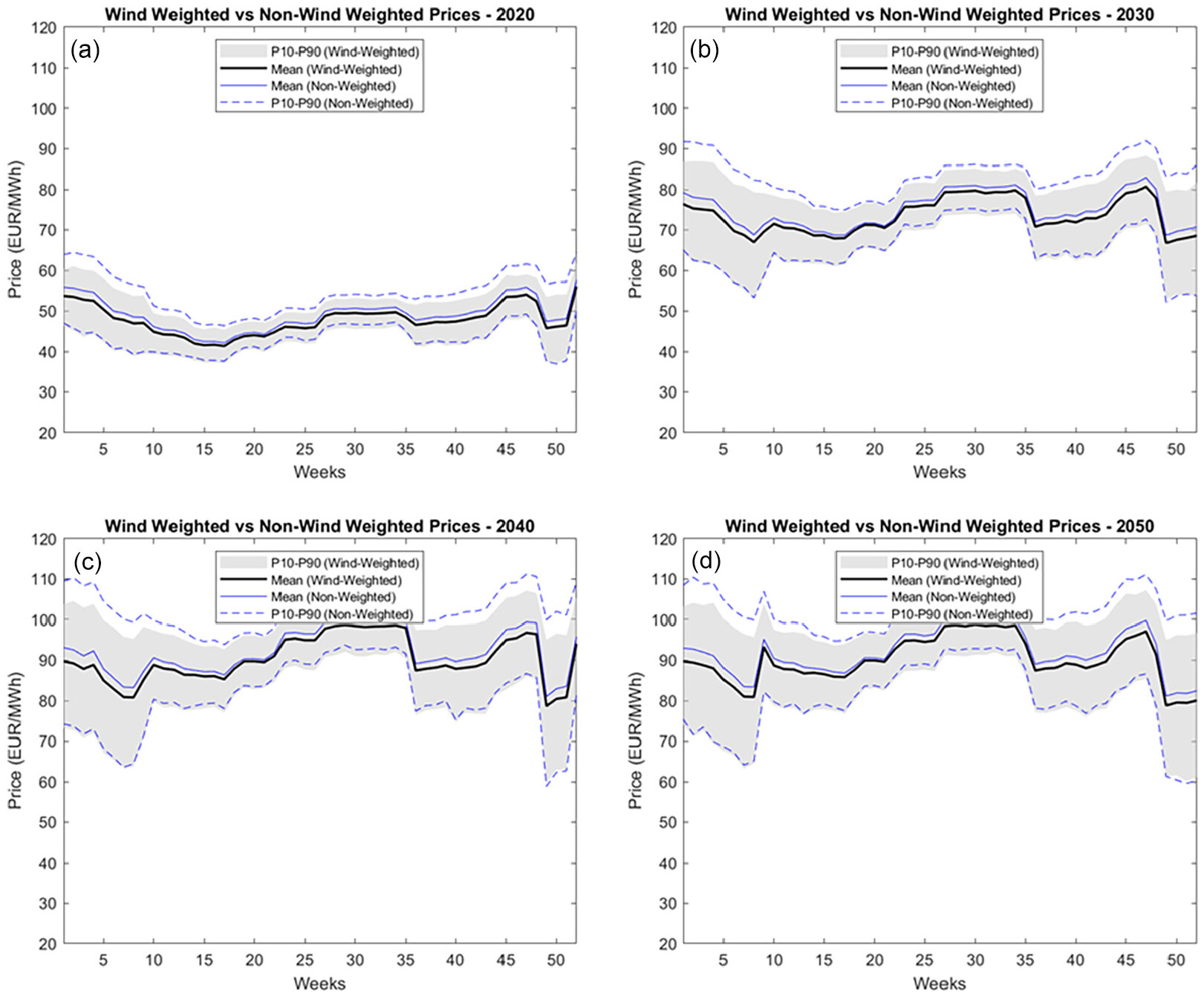

Kitzing et al. 2024), making it a stark contrast to the merchant revenue case.

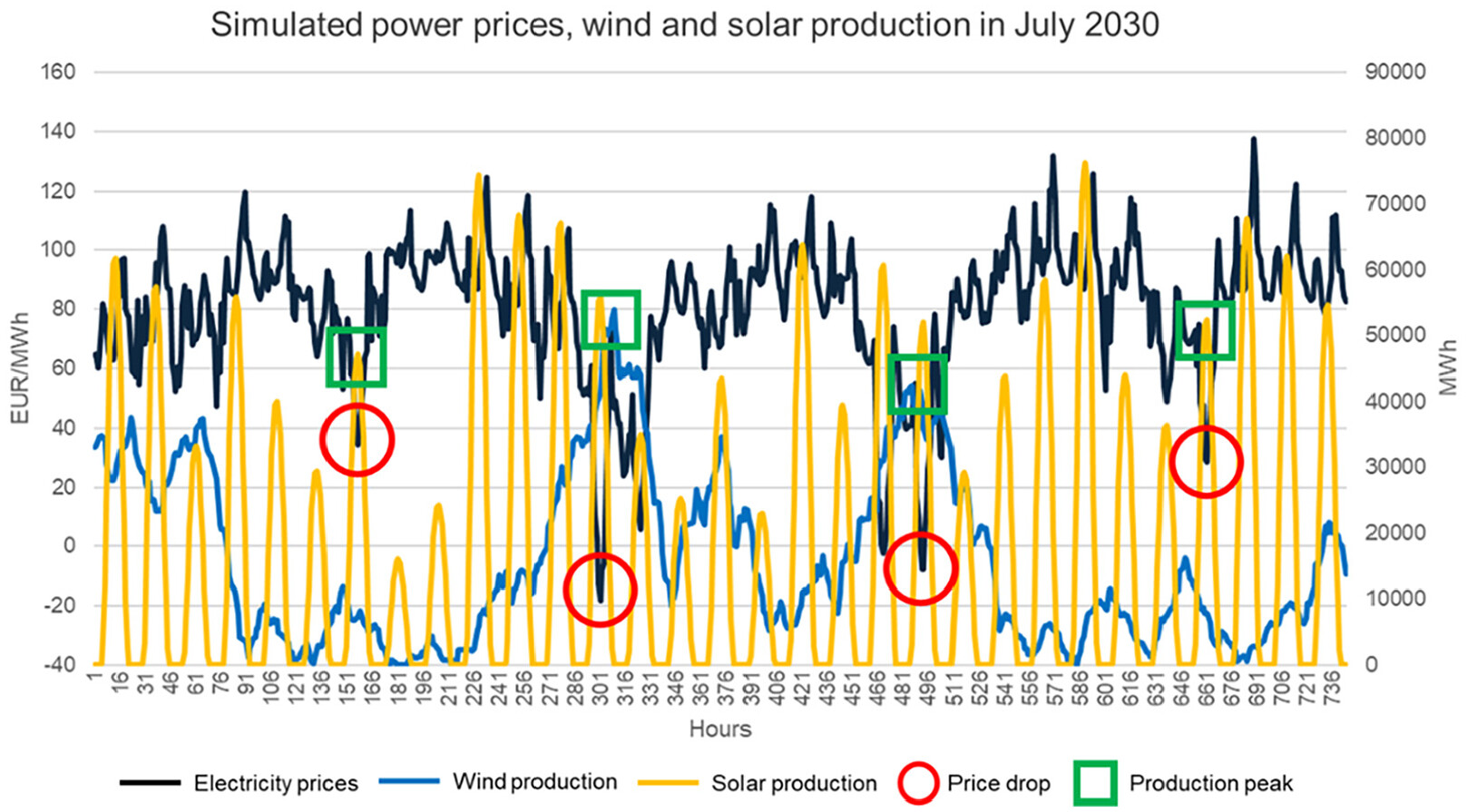

Our debt size quantification method consists of two steps. First, we generate revenues for an offshore wind farm under the two different payment schemes (merchant and two-sided CfD) by extending the hourly stochastic power-price model developed by

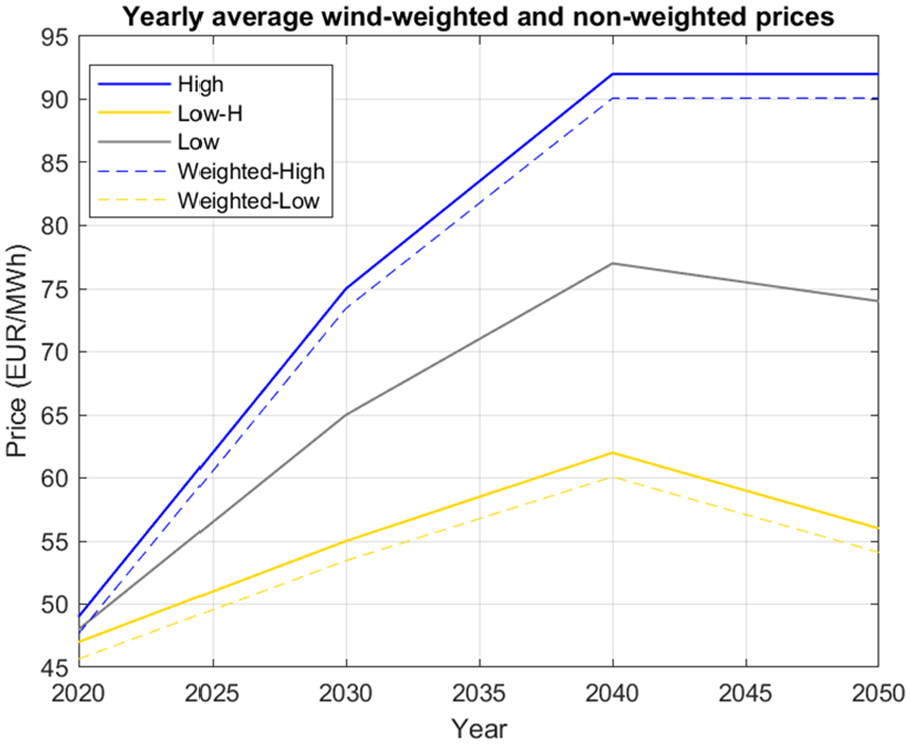

Keles et al. (2013). The model simulates stochastic hourly electricity prices for single years by learning from historical prices and their volatility. Further, it accounts for the price impacts of the expected future increase in solar and wind energy via the merit order effect. To generate long-term revenues, we model hourly price volatility around plausible future annual prices, derived from

Yilmaz et al. (2022), who simulate the European power system under assumptions of deep decarbonization and increasing carbon prices—a realistic future price projection, albeit one among many possible scenarios.

Second, we calculate shareholder value at different debt sizes using

Kitzing and Weber’s (2015) liquidity management model as a starting point. In doing so, we find the optimal capital structure at the debt size that maximizes shareholder value. Our study borrows from trade-off theory, suggesting that companies target a debt level that maximizes the benefits of leverage—the tax-deductibility of interest payments—until the potential financial distress costs of additional debt reduce the company’s value (

Kraus and Litzenberger 1973). Finally, we quantify the impact of our modeled two-sided CfD on electricity production costs, expressing its benefit to electricity consumers who bear the final cost of revenue stabilization.

Despite the growing literature on energy infrastructure finance, studies on renewables and the effect of remuneration mechanisms on debt size are limited. Several academic studies relate closely to our analysis.

Gohdes (2023) and

Gohdes et al. (2023) examine the bankability of different revenue mixes, comprising corporate Power Purchase Agreements (PPAs) and merchant revenues, under the bank’s debt covenants and capital structure constraints. Similarly,

Gohdes et al. (2022) and

Hundt, Jahnel and Horsch (2021) investigate the impact of different off-taker creditworthiness and merchant risk on onshore wind electricity production costs and project financing conditions, including debt size.

Mora et al. (2019) model the impact of wind speed uncertainty on debt size and electricity production costs, while

Ostrovnaya et al. (2020) estimate the impact of merchant risk on the WACC (weighted average costs of capital) for an onshore wind farm in the UK. Further,

Newbery (2016) examines the impact of introducing CfD as part of UK market reform (

Grubb and Newbery 2018) on reducing WACC for renewable energy generators. Other industry reports investigate the impact of merchant risk on RE financing (

Arup 2018;

Aurora Energy Research 2018;

Deloitte 2020;

Heiligtag et al. 2018;

Hern et al. 2013;

IEA 2021;

PwC 2020). However, they mostly quantify the effect on WACC, disregarding the impact on debt size and shareholder value.

•

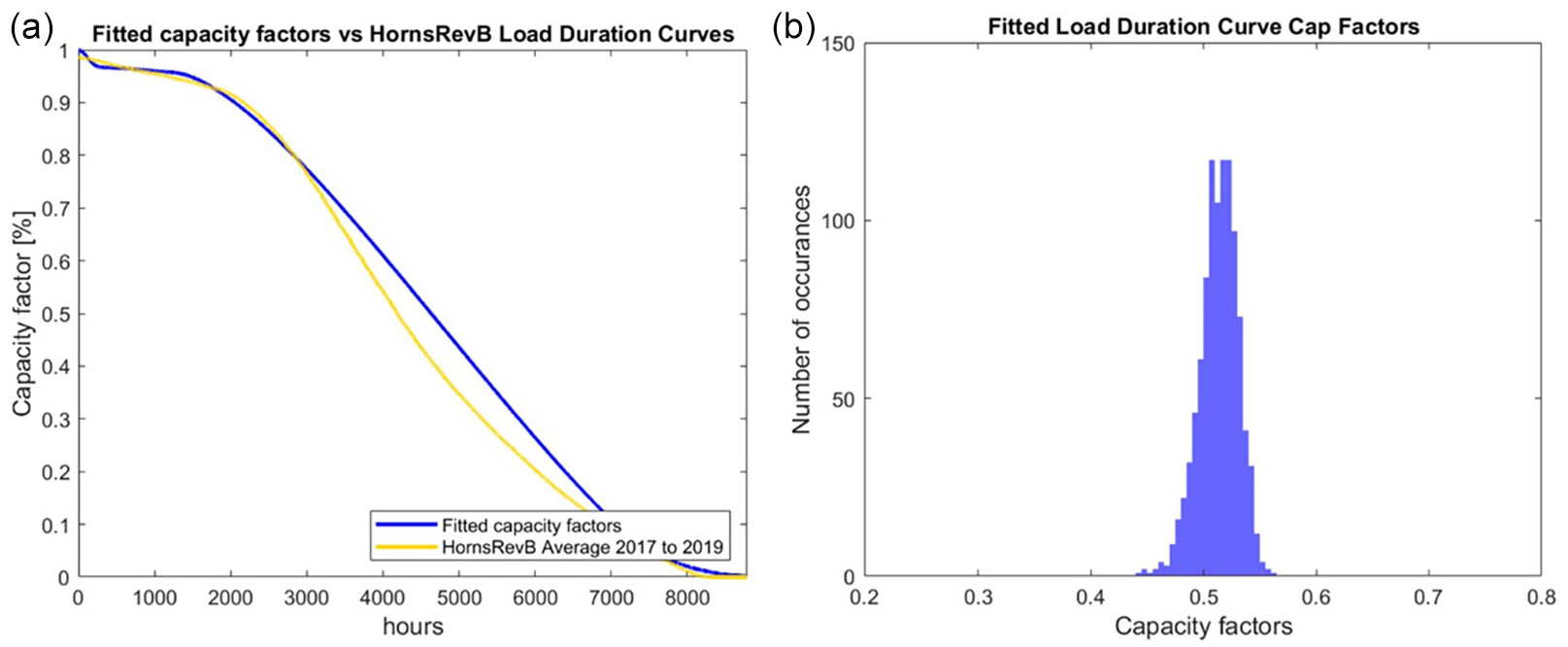

We extend the

Keles et al. (2013) stochastic wind-power production and power-price model to generate long–term revenues for an offshore wind farm. The

Keles et al. (2013) model simulates stochastic hourly price scenarios for one calendar year. As initially suggested by

Keles et al. (2012), we combine this model for the first time with long-term electricity price projections generated with the PERSEUS-EU.

•

We adjust

Kitzing and Weber’s (2015) liquidity management model to account for project financing, deviating from the original model version that assumed a corporate finance cash-flow structure. Furthermore, we define financial distress as occurring when the project violates its debt covenants, unlike

Kitzing and Weber (2015), who define financial distress as the liquidity account consisting of retained earnings and shareholder equity being negative. We combine the long-term revenues and the liquidity management model into one modeling framework to derive optimal debt size, considering financial distress caused by cash-flow volatility.

Third, by quantifying the effect of merchant risk on the capital structure of RE projects, we contribute to the ongoing policy debate on the future of support policies for renewables in Europe. We highlight the importance of revenue stabilization via a government-backed CfD or premium support scheme for maintaining favorable financing conditions for offshore wind investments.

We structure the remainder of the paper as follows. Section 2 provides a theoretical background supporting our modeling approach. Section 3 presents the modeling approach and our basic assumptions. Section 4 outlines the results of our analysis, compares them with earlier research, and critically reflects on our methods. Section 5 provides conclusions and recommendations for future work.

5. Critical Reflection and Discussion

Our study is the first to quantify the impact of merchant risk and revenue stabilization via CfDs on financial distress and debt sizing, adding to the dynamic discussion on CfD designs (

Kitzing et al. 2024). Nevertheless, there are several considerations regarding our study. First, we assess the impact of revenue stabilization via power purchase contracts. Notwithstanding other revenue risk mitigation mechanisms such as forward electricity contracts (

Woo, Horowitz and Hoang 2001) and option hedging involving financial settlements with financial counterparts (

Guidera and Jamshidi 2016), PPAs are the backbone of renewable energy financing. The question is who should bare the cost of risk mitigation. Our study assesses government-backed CfDs; however, other PPA mechanisms, such as contracts with corporates, exist in various forms (

Bruce et al. 2020;

Tang and Zhang 2019) and have been growing by 65 percent year on year since 2013 (

Bruce et al. 2020). Relying on corporate PPAs to deliver renewable energy capacity could replace the risk-mitigation role assumed by CfDs and save public finances (

Gohdes et al. 2023).

Government-held auctions are administrative processes, and as such, they might be organized inefficiently and lead to sub-optimal outcomes such as not procuring sea bed rights for the least cost or to the counterparty most capable of delivering the project in time (

Mora et al. 2017). While there is empirical evidence for this (see for instance,

Winkler, Magosch and Ragwitz 2018), it does not imply that corporate PPAs could completely substitute government-procured CfDs. The main reason is the capacity of the corporate PPA market to mitigate power price risks for the volume of offshore wind electricity Europe plants to deploy until 2050. Corporates with investment-grade credit ratings (above BBB- or Baa3, depending on the credit agency) and high and long-term demand for green electricity are limited in supply (

Beiter et al. 2023), making the financing of offshore wind farms contracted via corporate PPAs more expensive (

Gohdes et al. 2022;

Hundt, Jahnel and Horsch 2021). Furthermore, through organizing CfD auctions, governments control the renewable capacity build-out and provide incentives even when market conditions increase the cost of corporate procurement, such as supply chain bottlenecks and rising materials costs (

IEA 2023).

Second, implementing two-sided CfDs could have implications for energy markets, which go beyond the main research question of this study. Two-sided CfDs could enable easier access to financing offshore wind projects and, hence, a more active offshore wind market. Besides utilities and oil & gas companies, the biggest investors in offshore wind in Europe (

Đukan et al. 2023), higher revenue stability could attract investors with more conservative risk-return investment profiles, such as pension funds and insurance companies. The enhanced actor diversity might reduce the sector’s cost of capital, helping offshore wind become more cost-competitive. These institutional investors could invigorate project acquisitions and capital refinancing back into project developers’ balance sheets, a model known as farm-downs (

McKinsey & Company 2020). On the other hand, greater offshore wind penetration could induce revenue cannibalization as the ever-growing wind fleet suppresses electricity prices due to its correlated production profile (

Hirth 2013). While the two-sided CfD would hedge project owners against price drops (depending on negative price designs), it could suppress prices for other generators like solar PV (

López Prol, Steininger and Zilberman 2020), further reducing the profitability of merchant projects.

Third, our results hold in the absence of other variables that might impact debt size apart from electricity prices and the variability of production volumes. Besides the country and macroeconomic risks (

Roth, Brückmann et al. 2021), leverage also depends on regulatory and policy risks, technology failure, and curtailment risks (

Egli 2020;

Esty 2002), sponsor experience, and the project ownership structure among the involved parties (

Vaaler, James and Aguilera 2008). Further, it is worthwhile noting that we define debt size exogenously as the share of debt in total investment costs and use an annuity loan repayment schedule. Project finance practices typically sculpt the debt repayment schedule for RE investments and derive debt size from the project’s variable cash flows (

Đukan and Kitzing 2023;

Mora et al. 2019;

Stetter et al. 2020). By not adjusting debt repayments to the project’s cash flows, our approach enables us to stress-test the project to different debt levels and record financial distress situations where the project violates debt covenants.

Fourth, we also made some notable adjustments in applying the trade-off theory. Trade-off theory primarily concerns corporate finance settings. We simplify assuming a project company with just one asset generating revenues, disregarding the many other corporate factors, such as information asymmetry and agency conflicts (

Jensen and Meckling 1976;

Myers 1984;

Myers and Majluf 1984), that might also influence capital structure. Further, other constraints on banks’ lending might deviate from the optimal leverage derived via our approach inspired by trade-off theory. Moreover, while we account for tax shields by deducting interest expenses from taxable income, we do not explicitly quantify their value (

Koller et al. 2005). In addition, the expected distress costs typically equal the probability of distress multiplied by the distress costs, including direct costs such as legal advice and indirect costs such as lost reputation and missed investment opportunities (

Esty 2002). We simplify and model financial distress costs as cash flow liquidity required to avoid violating debt covenants.

Finally, the long-term price projection in this study is derived from

Yilmaz et al. (2022), who simulate an increasing electricity price trajectory driven by rising CO2 prices. This might come from the missing full-decarbonization approach, leaving some natural and synthetic gas-fueled generation capacities in the German energy system and driving electricity prices high. However, we acknowledge that this might be only one of the possible outcomes. At the same time, other price projections/scenarios in the literature foresee a decreasing trend in the long-run due to the increasingly renewables-dominated and finally fully decarbonized energy market (

Energienet 2018;

Liebensteiner, Ocker and Abuzayed 2025). It is worth mentioning that the underlying long-term price projection has only limited influence on our main conclusion, highlighting the need for de-risking mechanisms for better financial planning, as price volatility is the main parameter behind this finding.

We also acknowledge that different methods in the literature appropriately describe the stochasticity of electricity prices.

Ward, Green and Staffell (2019) argue that generators bid differently from their marginal costs for strategic reasons. The authors suggest a method to simulate the merit order based on multiple possible bidding behaviors, leading to price formation that differs from the SRMC approach. Nonetheless, the statistical model applied in this study has been validated by

Keles et al. (2012) and, more recently, by

Keles and Dehler-Holland (2022), with a good performance in simulating stochastic electricity prices. Further, our model does not directly capture curtailment; instead, it calculates lower capture prices by including negative price hours. This slightly decreases the reported capture prices compared to assuming that wind and solar producers would curtail at negative prices. However, since curtailment behavior is highly uncertain, depending not only on the contractual situation but also on the individual behavior of grid operators, we have chosen to exclude this from the analysis.

6. Conclusions

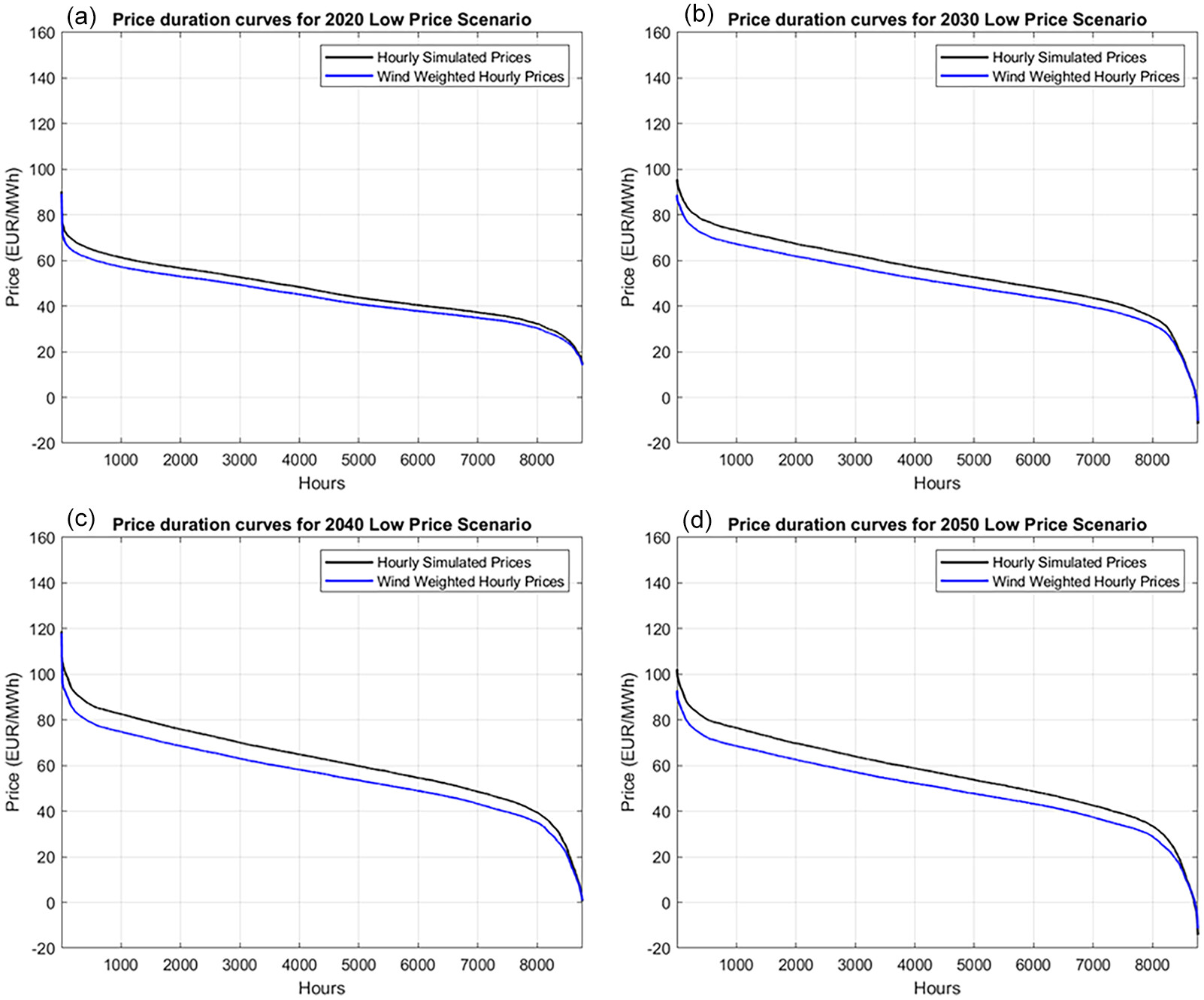

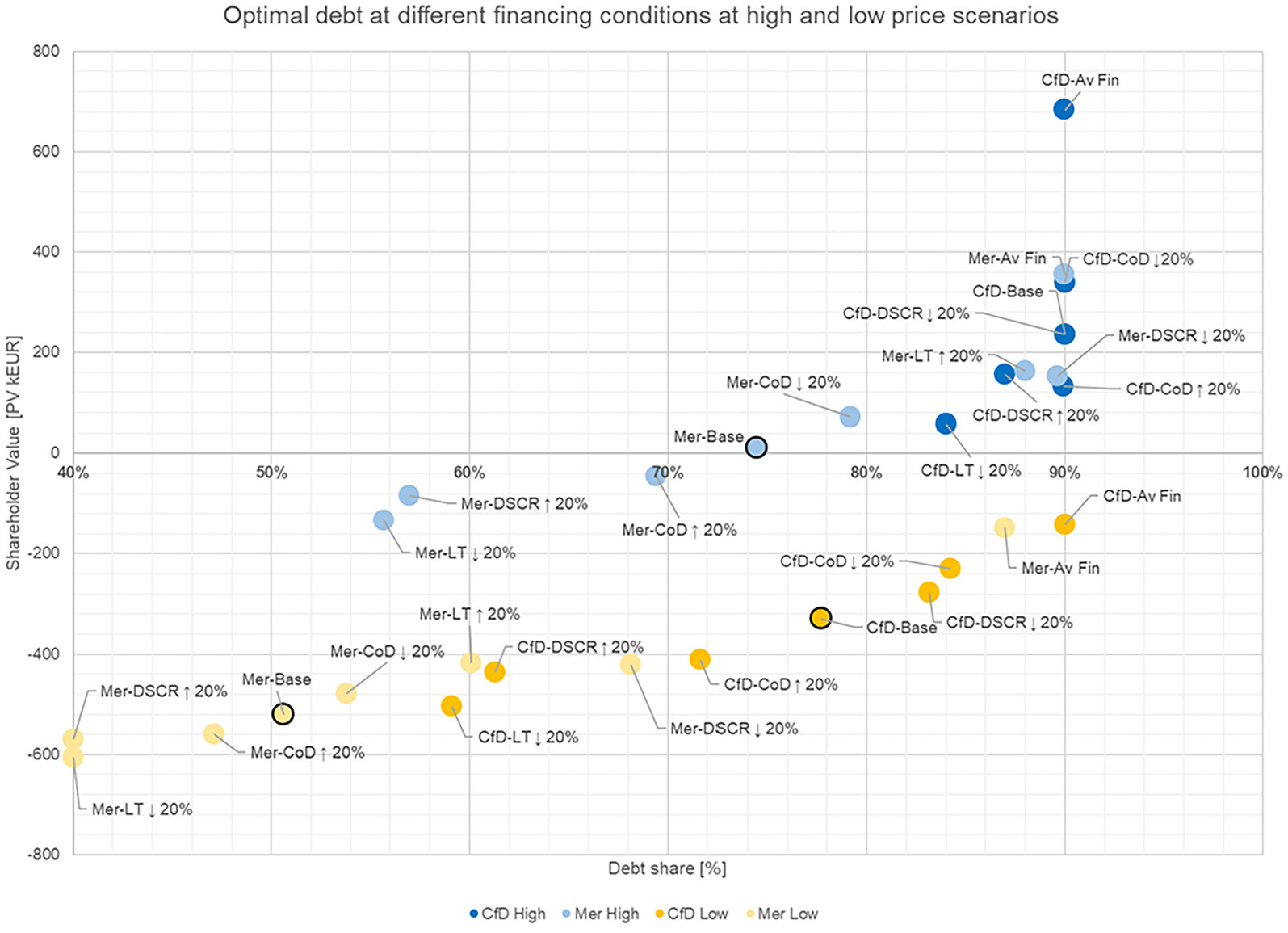

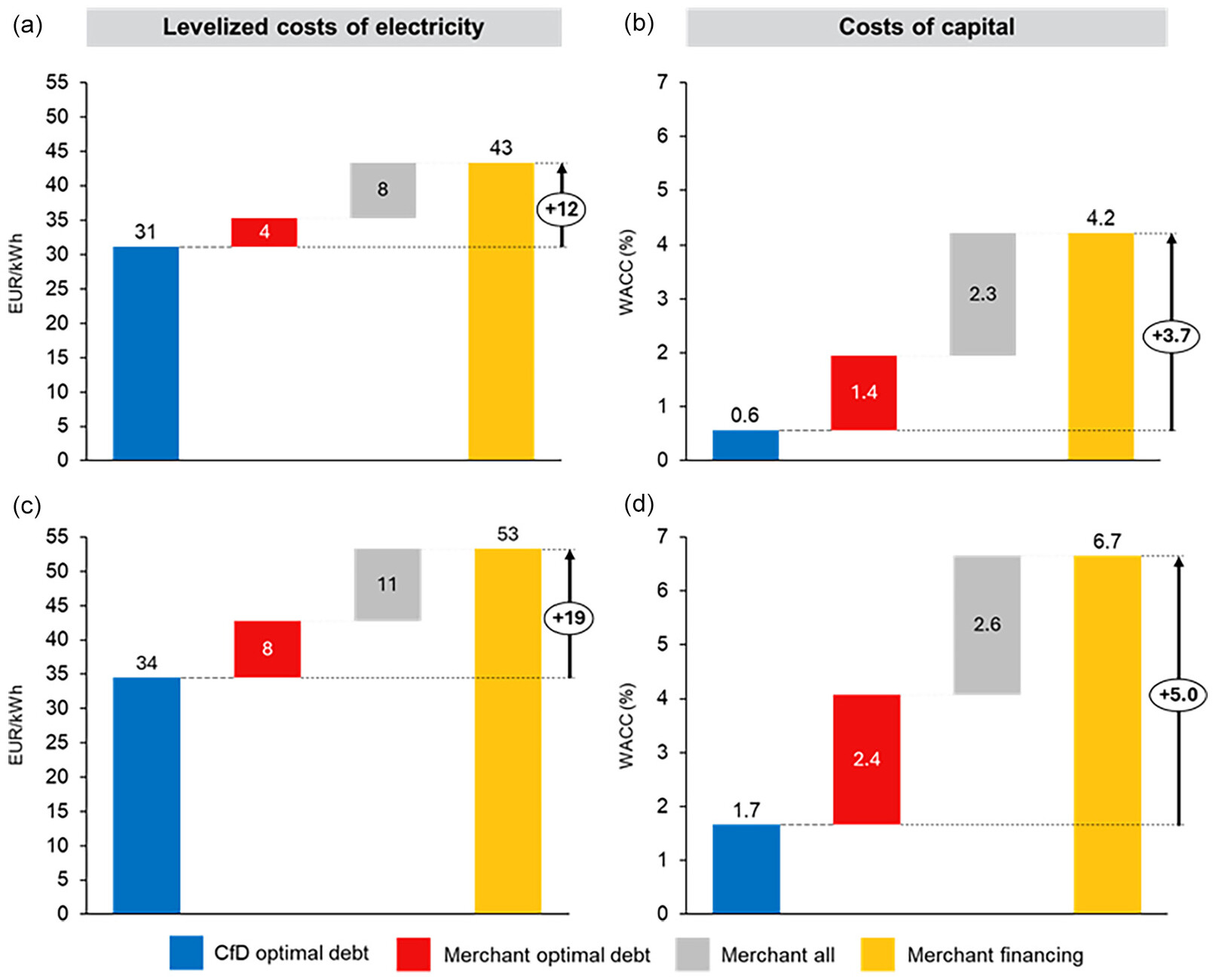

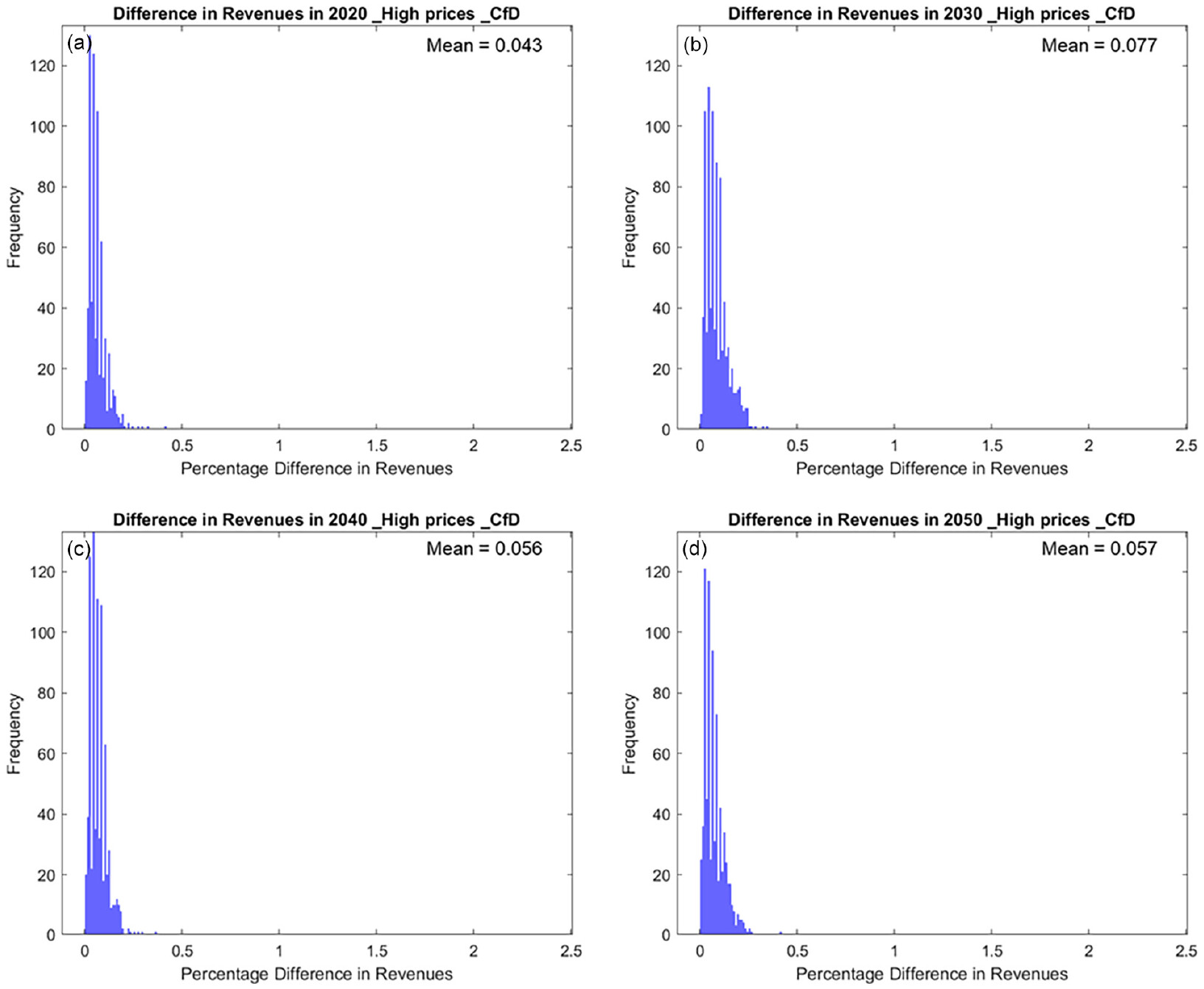

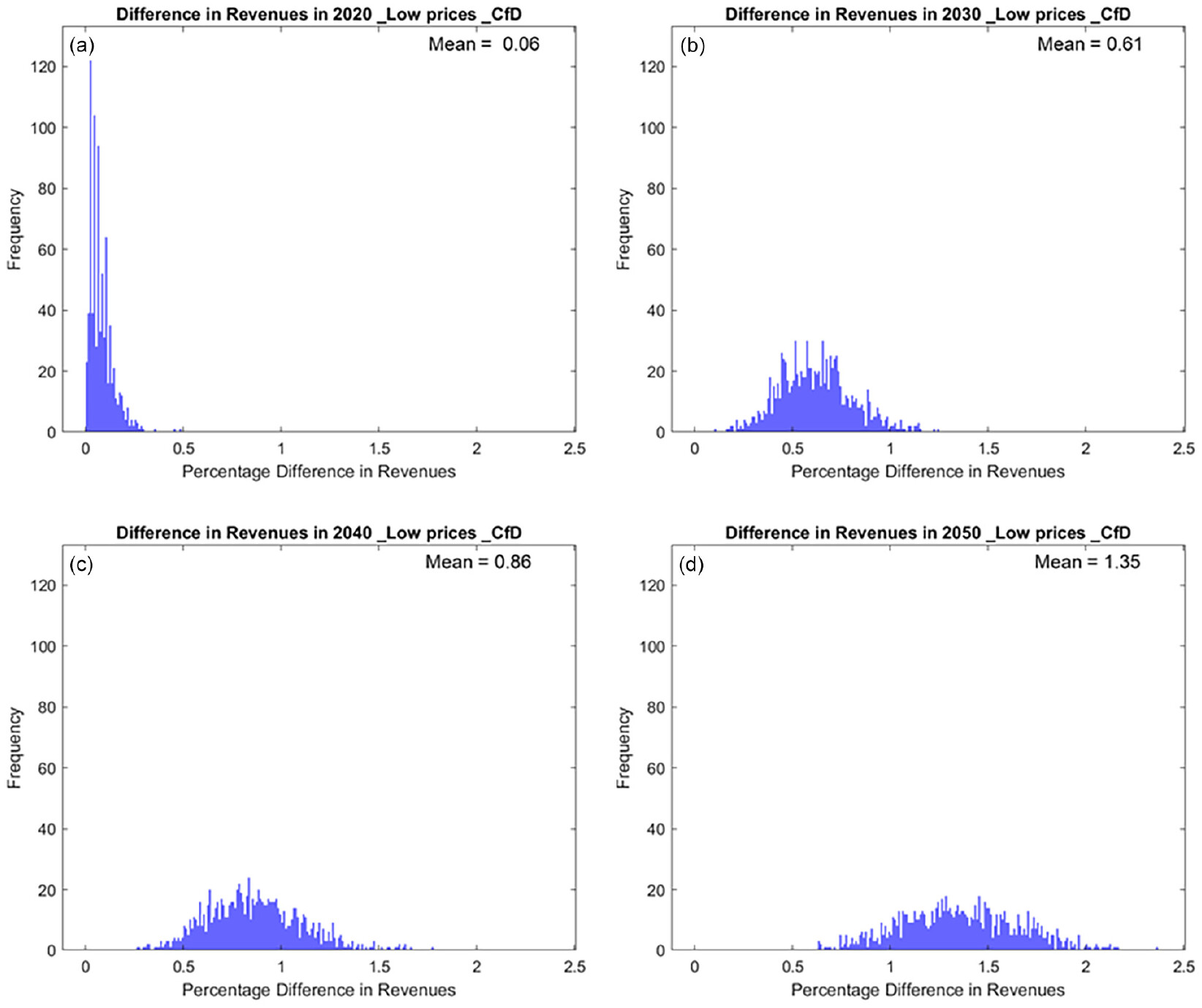

Our study quantifies the impact of revenue stabilization via two-sided CfDs on debt size by considering the impact of revenue variability on financial distress costs. While comparing a hypothetical offshore wind farm in the North Sea with two revenue scenarios—one with the CfD and another with fully merchant revenues—we find revenue stabilization to increase debt size by between 27 percent and 15 percent, depending on the power price scenario. The CfD project maximizes shareholder value at the highest measured debt size of 90 percent, while the merchant project does so at a gearing of 74 percent in an electricity price scenario where power prices reach 92 EUR/MWh in 2040. In an alternative electricity price setting with prices reaching 62 EUR/MWh, the difference between the projects is even larger, with optimal debt size at 77 percent for the CfD project and at 50 percent for the merchant project. We subsequently show that revenue stabilization could save electricity consumers between 12 to 18 EUR/MWh in electricity generation costs, depending on the power price scenario. Such savings could justify the government taking on revenue stabilization instead of leaving this to the private market via corporate PPAs. However, a more detailed investigation of the costs and benefits would be needed along the lines of

Gohdes et al. (2023). Our analysis also points out the impact of financing conditions on leverage. An improvement in the DSCR from 1.6 to 1.35, an increase in loan duration from 15 to 18 years, and a decrease in interest rates from 3.5 percent to 1.96 percent, increases optimal debt size by 36 pp for the merchant project in the low-price scenario, compared to a 0.44 pp increase from accounting for negative power prices.

These results highlight the importance of revenue stabilization mechanisms, showing for the first time their impact on debt size quantitatively and demystifying the debate (

Wind Europe 2018) on the implications of merchant risk on generation costs and financial distress. Revenue stabilization is crucial for helping Europe mobilize low-cost capital (

Klaaßen and Steffen 2023) to reach its ambitious offshore wind goals. Along those lines, future research could build upon this study and similar lines of research (

Gohdes 2023;

Gohdes et al. 2022,

2023) and investigate in more detail the impacts of specific CfD designs (

Kitzing et al. 2024). The analysis could deal with both the risk to the bidder and the government that bears the risk of CfD payments. In the wake of soaring electricity prices in 2023 (

DG Energy 2023), European governments have started realizing the benefits of CfDs for producers and electricity consumers. However, questions regarding their most optimal design and the impacts of this on renewables rollout, risk, and financing remain.