Effectiveness of Green Financing Activities and Performance Management on Banking Sector: An Empirical Study

Abstract

1 Introduction

1.1 Research Contribution

1.2 Research Objectives

1.3 Research Question RQ1

RQ2: Is there any relationship between green financing activities and the financial flow level of the banking sector?

2 Literature Review

| Authors/ | Research | |||

|---|---|---|---|---|

| Citation | sources | methods | Study's aim | Findings |

| Xu et al. (2020) | Hengjie Xu, Qiang Mei et al. | Meta-analytic approach | To examine the connection between green financing and business sustainability performance. | Enterprise green effectiveness and discover a strong association between good green business practices and sustainable funding. |

| Rehman et al. (2021) | Alam Rehman et al. | Structural equation modeling | To investigate the connections among several factors. | The accomplishment of green banking practices is significantly influenced by policy, daily operations, and investments. |

| Kalyar et al. (2020) | Masood Nawaz, Kalyar et al. | Convenient Sampling | Details were acquired through 238 textile businesses in Pakistan's Punjab region. | The economic success of enterprises is significantly impacted directly by GSCM operations as well as implicitly by their contribution to the environment. |

| Zheng et al. (2021) | Guang-Wen, Zheng et al. | Structural equation modeling | To inspect the components of green finance and how they affect financial institutions’ sustainability performance in emerging markets like Bangladesh | Features of green lending from a societal, economic, and ecological perspective all benefited banks’ sustainability results significantly. |

| Guang-Wen and Siddik (2023) | Zheng Guang–Wen and Abu Bakkar Siddik | Structural equation modeling | Look into the connection between GI, GF, and EP during the COVID-19 outbreak and Fintech adoption (FA). | FA has major consequences on GI, GF, and EP, while GF greatly enhances EP and GI. |

| Yan et al. (2022) | Chen Yan et al. | Structural Equation modeling | The adoption of fintech affects the resource efficiency of economic firms in a developing nation. | The interaction between the embrace of FinTech and banking organizations is successfully mitigated by innovations in green and sustainable finance. |

| Chen et al. (2022) | Jing Chen et al. | Structural equation modeling | To investigate how GB practices, affect Bangladeshi private commercial banks (PCBs) green finance sources and environmental performance. | Bank employees, workflow, and strategy-related GB initiatives had considerable advantages for sustainable finance, in contrast to client-related GB practices, which were not substantial. |

| Zhang et al. (2022) | Xin Zhang et al. | Convenient sampling technique | To gather the most important data from Bangladeshi PCB bankers. | Sustainable banking practices considerably raise banks’ options for green finance and their ecological sustainability. |

| Ellahi et al. (2023) | Anum Ellahi et al. | Structural Equation Model | To identify the progress of green banking practices in the banking sector | Education appears to have a significant positive impact on green banking awareness in the selected sample. |

| Taneja and Özen (2023) | S Taneja and E Özen | Convenience sampling | To evaluate the impact of green finance initiatives on bank performance in terms of environmental protection. | The study recommended that banks support the use of sustainable environmental technology as it is critical to improving bank performance and reputation in the minds of clients. |

| Gulzar et al. (2024) | Rafia Gulzar et al. | Structural equation modeling | To investigate the significant influence that green banking policies have on banks’ environmental performance | The study emphasizes the positive impact of green banking on employee practices, operational procedures, customer engagement, and policy adherence, contributing significantly to the promotion of green finance. |

| Gulzar et al. (2024) | Rafia Gulzar et al. | Partial least squares structural equation modeling | To investigate the profound impact of green banking practices on bank environmental performance | The study emphasizes the positive impact of green banking on employee practices. |

2.1 Related Works

2.2 Research Gap

2.3 Theoretical Framework

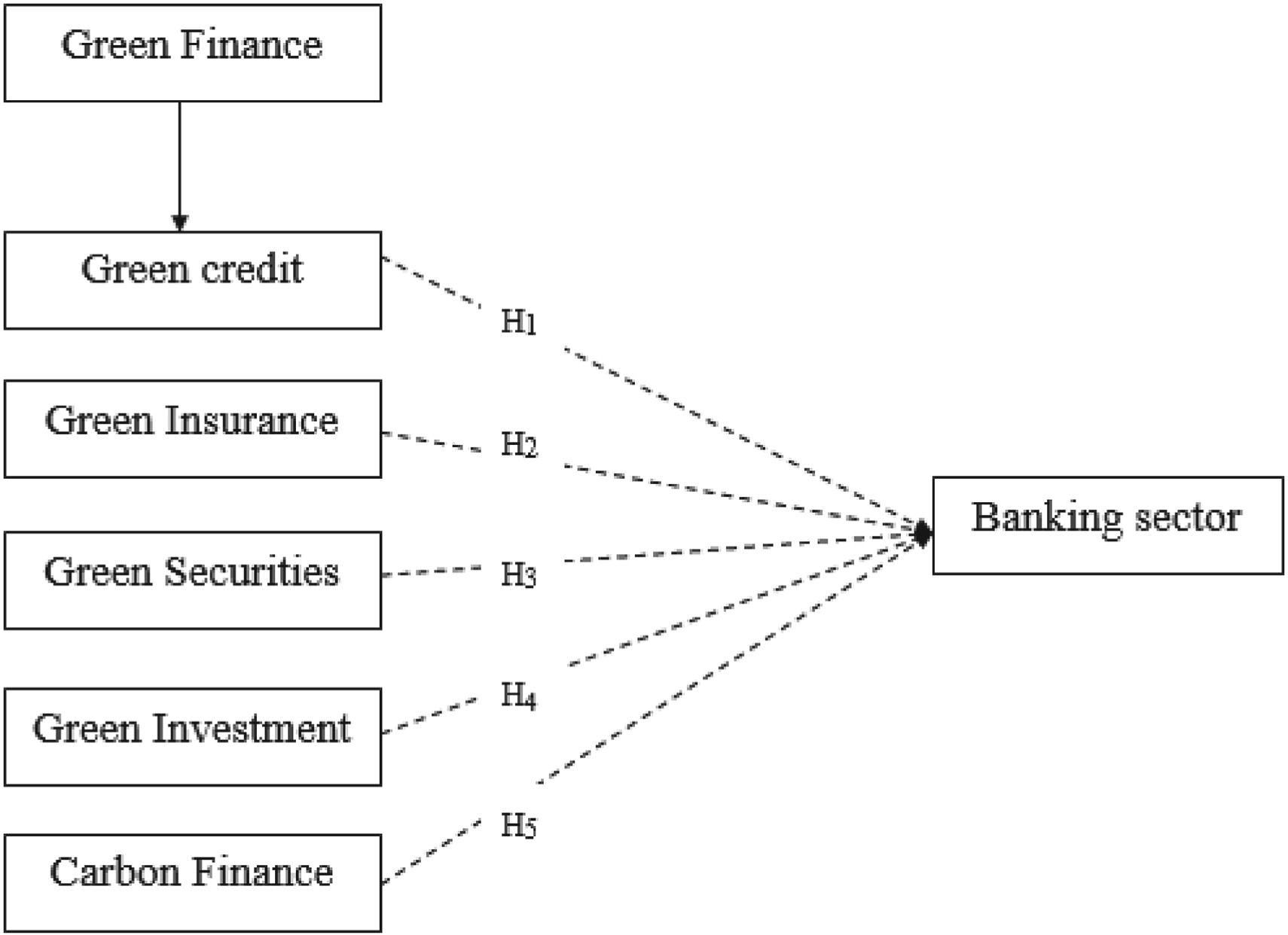

2.4 Hypothesis Development and Conceptual Model

H1: Green credit significantly impacts the financial flow levels.

H2: Green insurance impacts the financial flow levels.

H3: Green securities directly impact the financial flow levels.

H5: Carbon finance impacts the financial flow levels.

3 Research Methodology

3.1 Variables Description

3.2 Data Collection

3.2.1 Sampling Technique

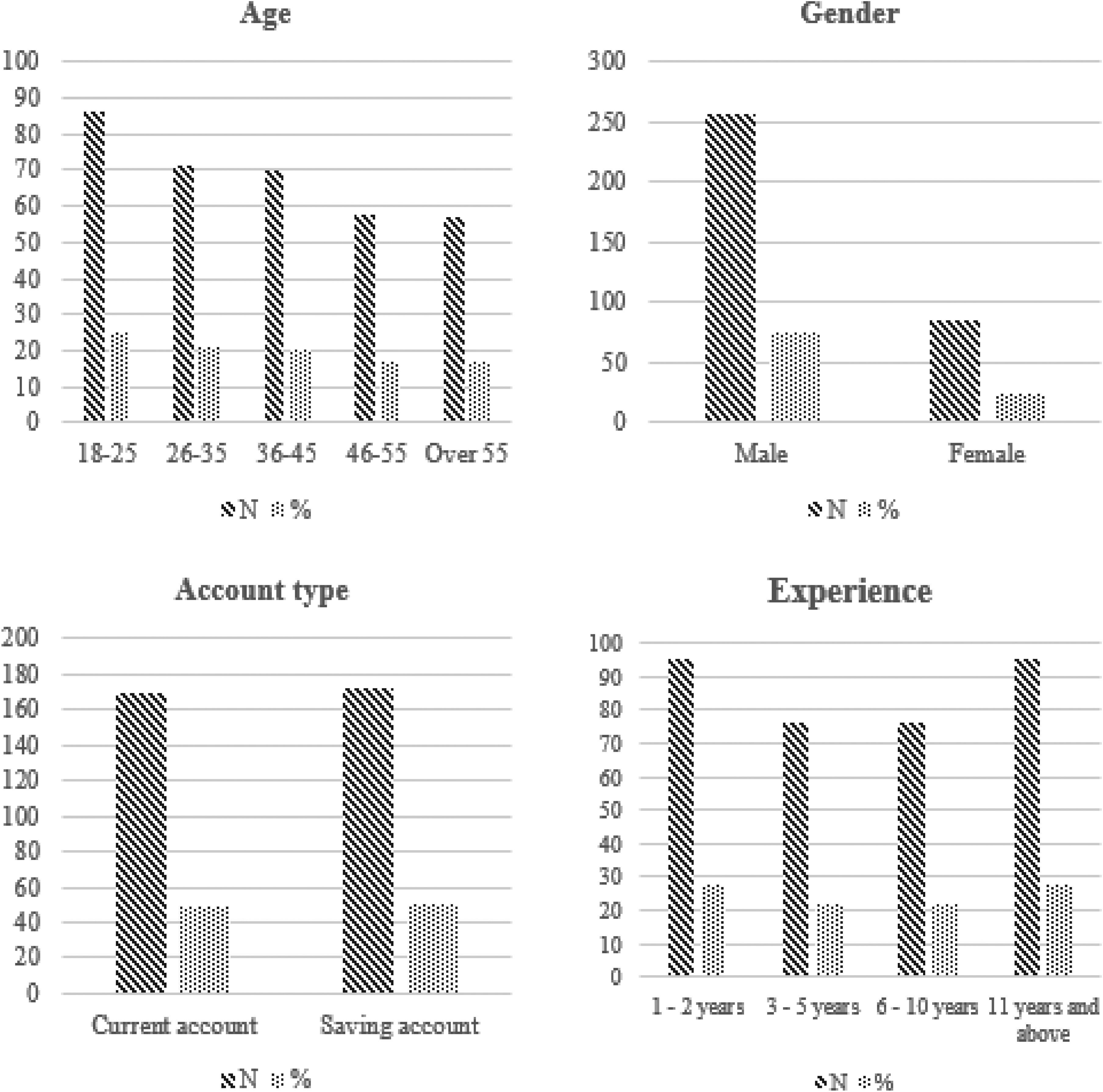

3.2.2 Sample Description

| Measures | Constructs |

|---|---|

| Green credit | Developed to assist in reducing climate change |

| Encourages ecologically responsible behavior | |

| Monitor and control the usage of services and products. | |

| Increase the number of resources accessible for the operations. | |

| Maintain the viability of the ecosystem. | |

| Green insurance | Sustainable transition claims are supported. |

| Design components for residence insurance and flexibility | |

| Green strategy components are included. | |

| Altering Insurance to be more sustainable | |

| Create a culture that is tolerant of risk. | |

| Green securities | Adapting climate finance solutions |

| Allowing the idea of sustainable development into practice | |

| Providing a financial incentive to address important social concerns | |

| Promote green commercial initiatives. | |

| Helps in opening up debt capital markets to financing | |

| Green investment | Diverse portfolios with greater responsibility |

| Financial risk is lower. | |

| Expanding carbon markets quickly | |

| Build forth favorable public perception. | |

| Earn substantial returns | |

| Carbon finance | Reducing carbon emissions worldwide |

| Encourage business growth and offer opportunities. | |

| Successfully spreads the co-benefits philosophy. | |

| Mitigating climate change's overall effects | |

| Purchase carbon credits produced by green initiatives. | |

| Financial flow levels | Provide customers with prompt service. |

| Offering the services at the time specified | |

| Flexible hours of operation | |

| Transactions are safe. | |

| Express enthusiasm for problem-solving |

3.2.3 Questionnaire Design

3.3 Research Design

4 Data Analysis and Interpretation

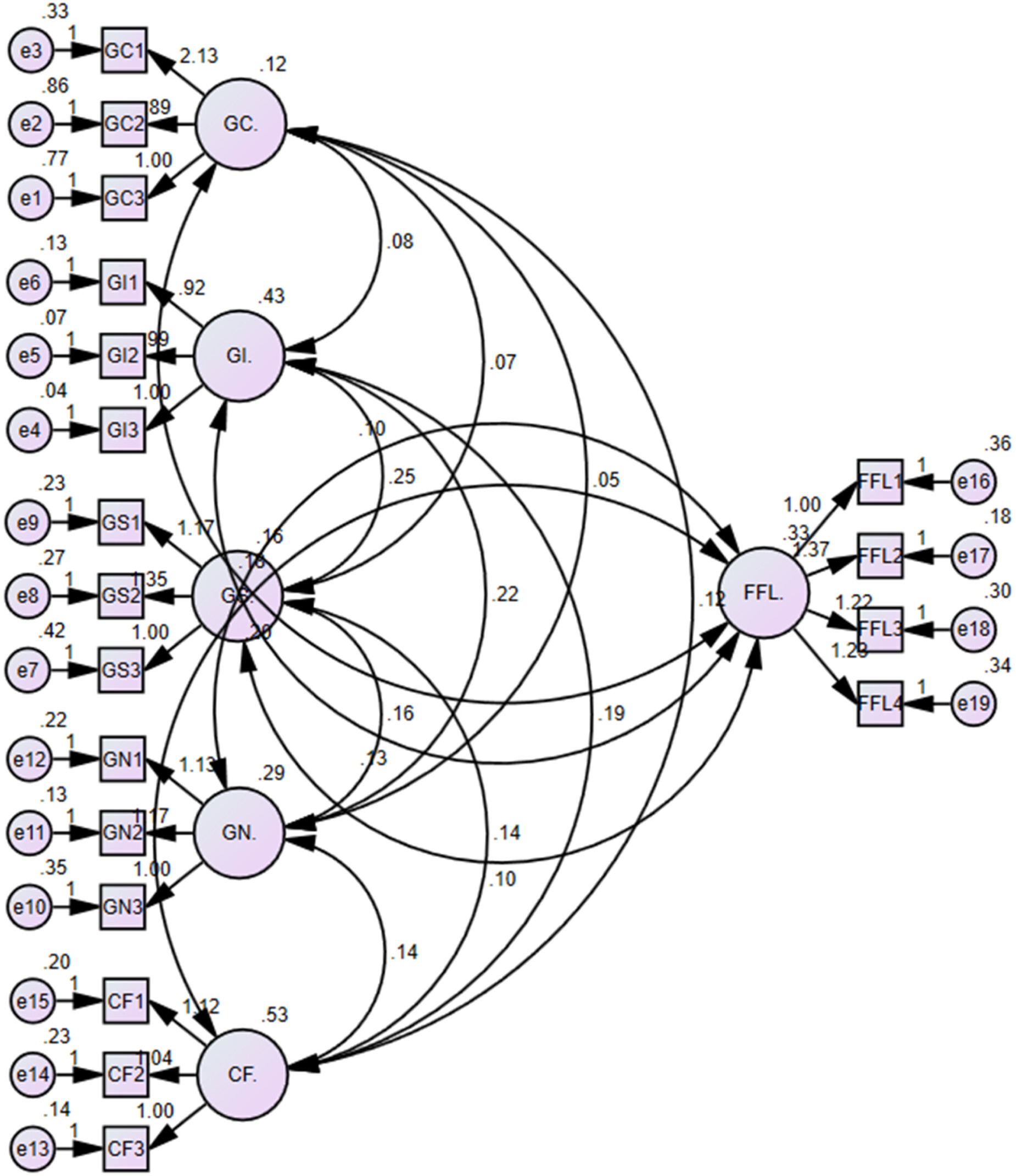

4.1 Measurement Model

| GC | GI | GS | GN | CF | FFL | |

|---|---|---|---|---|---|---|

| GC1 | 0.694 | |||||

| GC2 | 0.853 | |||||

| GC3 | 0.783 | |||||

| GI2 | 0.815 | |||||

| GI3 | 0.809 | |||||

| GI4 | 0.780 | |||||

| GS1 | 0.775 | |||||

| GS2 | 0.816 | |||||

| GS3 | 0.832 | |||||

| GN3 | 0.698 | |||||

| GN4 | 0.816 | |||||

| GN5 | 0.864 | |||||

| CF3 | 0.991 | |||||

| CF4 | 0.733 | |||||

| CF5 | 0.714 | |||||

| FFL1 | 0.859 | |||||

| FFL2 | 0.816 | |||||

| FFL3 | 0.847 | |||||

| FFL4 | 0.815 |

| Measures | Items | Loadings | CR | α | AVE |

|---|---|---|---|---|---|

| Green credit (GC) | GC1 | 0.714 | 0.724 | 0.715 | 0.606 |

| GC2 | 0.859 | ||||

| GC3 | 0.816 | ||||

| Green insurance (GI) | GI2 | 0.847 | 0.932 | 0.936 | 0.738 |

| GI3 | 0.819 | ||||

| GI4 | 0.778 | ||||

| Green security (GS) | GS1 | 0.816 | 0.765 | 0.768 | 0.692 |

| GS2 | 0.864 | ||||

| GS3 | 0.799 | ||||

| Green investment (GN) | GN3 | 0.796 | 0.823 | 0.813 | 0.532 |

| GN4 | 0.733 | ||||

| GN5 | 0.808 | ||||

| Carbon finance (CF) | CF3 | 0.775 | 0.887 | 0.900 | 0.754 |

| CF4 | 0.816 | ||||

| CF5 | 0.832 | ||||

| Financial flow levels (FFLs) | FFL1 | 0.872 | 0.868 | 0.863 | 0.618 |

| FFL2 | 0.782 | ||||

| FFL3 | 0.734 | ||||

| FFL4 | 0.766 |

| GC | GI | GC | GN | CF | FFL | |

|---|---|---|---|---|---|---|

| Hetero–Monotrait (HTMT) | ||||||

| GC | ||||||

| GI | 0.415 | |||||

| GC | 0.546 | 0.477 | ||||

| GN | 0.534 | 0.697 | 0.597 | |||

| CF | 0.776 | 0.563 | 0.798 | 0.864 | ||

| FFL | 0.578 | 0.697 | 0.827 | 0.574 | 0.748 | |

| Fornell–Larcker criterion (FLC) | ||||||

| GC | 0.778 | |||||

| GI | 0.359 | 0.859 | ||||

| GC | 0.494 | 0.933 | 0.831 | |||

| GN | 0.264 | 0.615 | 0.722 | 0.729 | ||

| CF | 0.480 | 0.406 | 0.483 | 0.369 | 0.868 | |

| FFL | 0.883 | 0.338 | 0.430 | 0.309 | 0.431 | 0.786 |

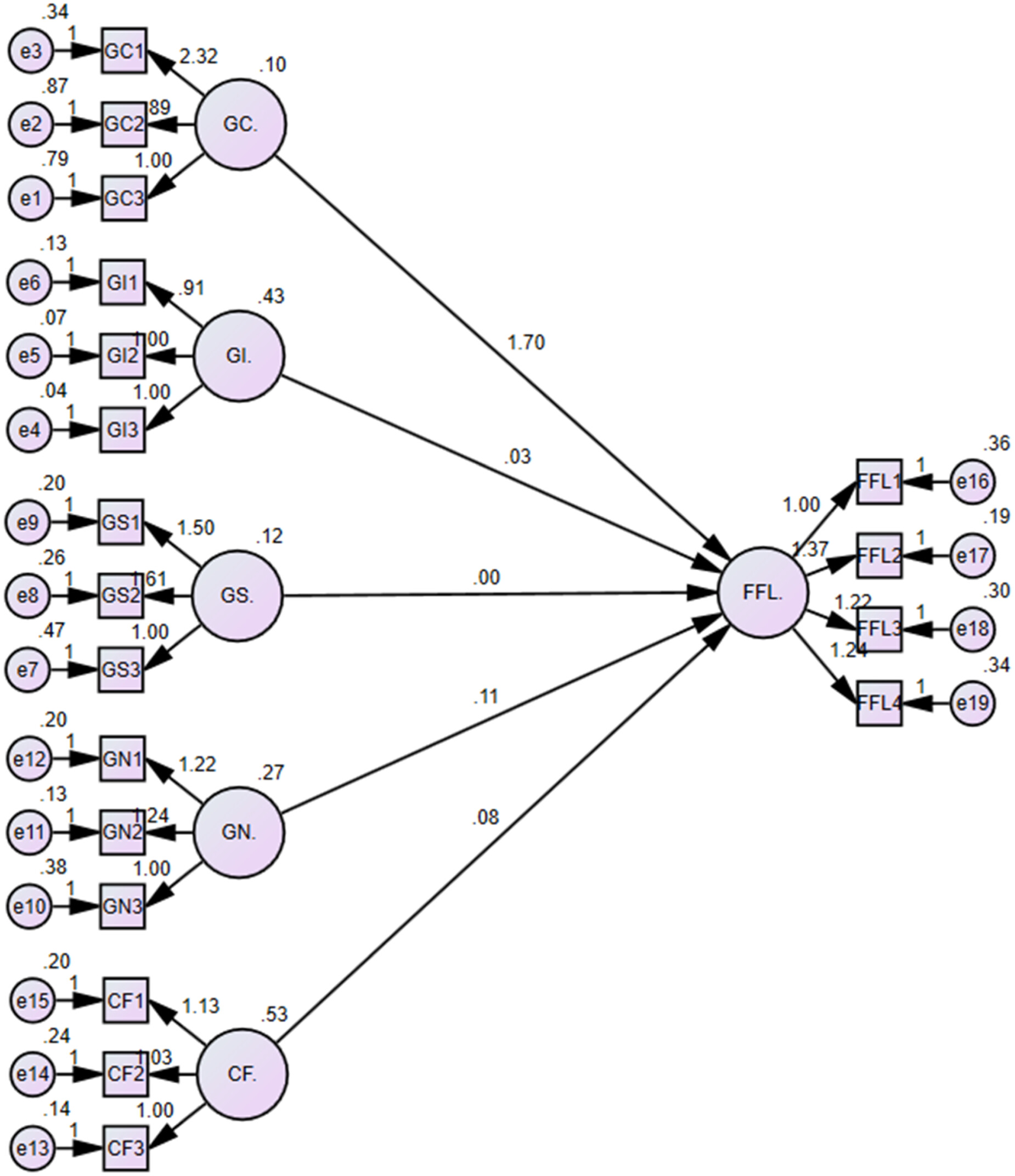

4.2 Structural Model

| Unstandardized | Standardized | ||||||

|---|---|---|---|---|---|---|---|

| coefficients | coefficients | ||||||

| Relation | Hypothesis | B | std. error | β | t | Sig. | Remark |

| GC→FFL | H1 | .587 | .059 | .487 | 9.913 | .000 | Accepted |

| GI→FFL | H2 | −.091 | .078 | −.076 | −1.16 | .247 | Rejected |

| GS→FFL | H3 | −.043 | .106 | −.033 | −.406 | .685 | Rejected |

| GN→FFL | H4 | .216 | .090 | .175 | 2.403 | .017 | Accepted |

| CF→FFL | H5 | .192 | .049 | .199 | 3.936 | .000 | Accepted |

4.3 Discussion

5 Conclusion, Suggestions, and Limitations

5.1 Conclusion

5.2 Suggestion and Study Implications

5.2.1 Practical Implications

5.2.2 Theoretical Implications

5.3 Limitations and Future Research

Declaration of Conflicting Interests

Funding

References

Biographies

Cite

Cite

Cite

Download to reference manager

If you have citation software installed, you can download citation data to the citation manager of your choice

Information, rights and permissions

Information

Published In

Keywords

Article versions

Authors

Metrics and citations

Metrics

Publication usage*

Total views and downloads: 3436

*Publication usage tracking started in December 2016

Publications citing this one

Receive email alerts when this publication is cited

Web of Science: 3 view articles Opens in new tab

Crossref: 3

- Assessing the effect of green disclosure on profitability and firm value in Indonesian Islamic banks

- Internal organisational value systems, green banking practices and firm performance: empirical evidence from banks

- The Impact of Green Banking Practice on Service Quality: Mediating Effect of Green Awareness and Green Image

Figures and tables

Figures & Media

Tables

View Options

View options

PDF/EPUB

View PDF/EPUBAccess options

If you have access to journal content via a personal subscription, university, library, employer or society, select from the options below:

I am signed in as:

View my profileSign out

I can access personal subscriptions, purchases, paired institutional access and free tools such as favourite journals, email alerts and saved searches.

loading institutional access options

Alternatively, view purchase options below:

Purchase 24 hour online access to view and download content.

Access journal content via a DeepDyve subscription or find out more about this option.